For Tax Pros: How to Actually Calculate Gift Tax Under IRC §2502 (2025 Edition)

The Step-by-Step Math Behind “No Gift Tax Due”

Most of the time, gift tax feels theoretical.

With the basic exclusion amount at $13.99m for 2025, almost no clients will ever write an actual check to the IRS for gift tax.

For most returns, the workflow is simple: file Form 709, burn some exemption, move on.

Once you start working with ultra–high-net-worth clients, that simplicity often breaks down.

I recently worked with a baller ophthalmologist whose net worth exceeded $100 million. Over his lifetime, he expects to transfer more than $50 million using a mix of spousal lifetime access trusts (SLATs), dynasty trusts, outright gifts, and significant charitable giving.

For clients like him, “no gift tax due” is not something you assume.

It’s something you must prove— by doing the math correctly under IRC §2502.

Below is a clean, repeatable framework you can use to calculate gift tax properly, even when the final answer is zero.

Example: The Grinch-Taxtor Becomes a Philanthropist (2025)

Assume the following:

Taxtor makes three gifts in the same year:

$10,000,000 cash to his spouse

$10,000,000 cash to the Red Cross

$10,000,000 cash to Kanye

Taxtor has never made any prior taxable gifts.

Step 1: Add Up All Gifts

Start with the total value of all transfers made during the year.

$10,000,000 to spouse

$10,000,000 to charity

$10,000,000 to Kanye

Total gifts: $30,000,000

Step 2: Apply the Annual Exclusion Under §2503(b)

Each transfer is a gift of a present interest, so each qualifies for the annual exclusion.

Annual exclusion for 2025: $19,000 per donee

Three donees × $19,000 = $57,000

$30,000,000 − $57,000 = $29,943,000

This is your starting point before deductions.

Step 3: Apply the Marital Deduction Under §2523 (Coordinated by §2524)

The spousal gift qualifies for the marital deduction (assuming a U.S. citizen spouse). However, you don’t get a double benefits for the same dollars. §2524 coordinates the rules and prevents applying both the annual exclusion and the marital deduction to the same portion of a gift.

Spousal gift: $10,000,000

Less annual exclusion: $19,000

Allowable marital deduction: $9,981,000

Applying the marital deduction to the taxable gift calculated thus far:

$29,943,000 − $9,981,000 = $19,962,000

Step 4: Apply the Charitable Deduction Under §2522 (Also Coordinated with §2524)

The same coordination logic applies to charitable gifts.

Charitable gift: $10,000,000

Less annual exclusion: $19,000

Allowable charitable deduction: $9,981,000

Applying the charitable deduction:

$19,962,000 − $9,981,000 = $9,981,000

This amount is the taxable gift for the year.

Step 5: Add Prior Taxable Gifts

Taxtor has no prior taxable gifts.

Cumulative taxable gifts: $9,981,000

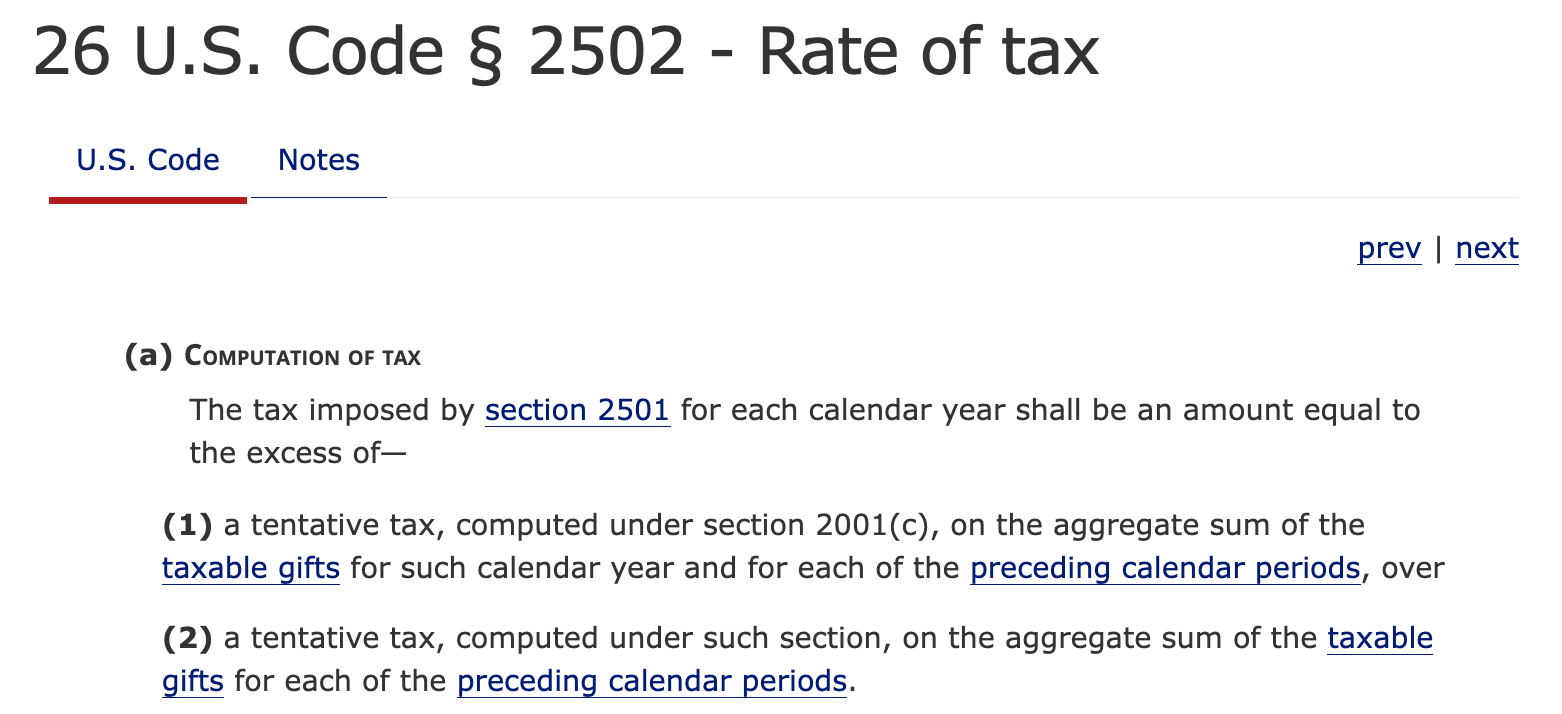

Step 6: Compute the Tentative Tax Under §2502

Next, compute gift tax on cumulative taxable gifts using the unified rate schedule.

Tax on first $1,000,000 (graduated): $345,800

Tax on remaining $8,981,000 at 40%: $3,592,400

Tentative tax:

$345,800 + $3,592,400 = $3,938,200

This is the tentative gift tax before applying the unified credits under §2505.

Step 7: Subtract Gift Tax Paid on Prior Gifts

There are no prior gifts and therefore no prior gift tax paid.

Tentative tax remains: $3,938,200

Step 8: Apply the Unified Credit

The unified credit is the saving grace Congress gave us. It can be used to offset gift tax liability dollar-for-dollar

Unified Credit for 2025: $5,541,800

Gift tax liability:

$3,938,200 − $5,541,800 = $0

Final Result

Even though Taxtor transferred $30 million in a single year:

Annual exclusions reduced the starting amount

The marital deduction eliminated the spousal gift

The charitable deduction eliminated the charitable gift

Only $9.981 million was taxable

The unified credit fully offset the tentative tax

Final gift tax due: $0

Why This Matters for Tax Pros

When a big-shot clients make multiple gifts across different categories in the same year, you cannot shortcut the analysis by saying “it’s under the exemption.”

The statute requires you to:

Determine taxable gifts

Apply deductions in the correct order

Compute tentative tax under §2502

Account for prior gifts

Then apply the unified credit

Once a client has prior taxable gifts, this same framework still applies. You simply plug the cumulative numbers into Steps 5 and 7.

and one final reminder: When you do this time-consuming math - make sure you charge for your time and expertise!

Tax Pros:

Have you dealt with a complicated gift-tax situation that required you to use this framework? If so, let’s share notes and learn from each other.