“Same Pain. Same Case. Different Wording… $200,000 Tax Difference”

Why lawsuit settlements are taxed based on how they’re written—not what actually happened

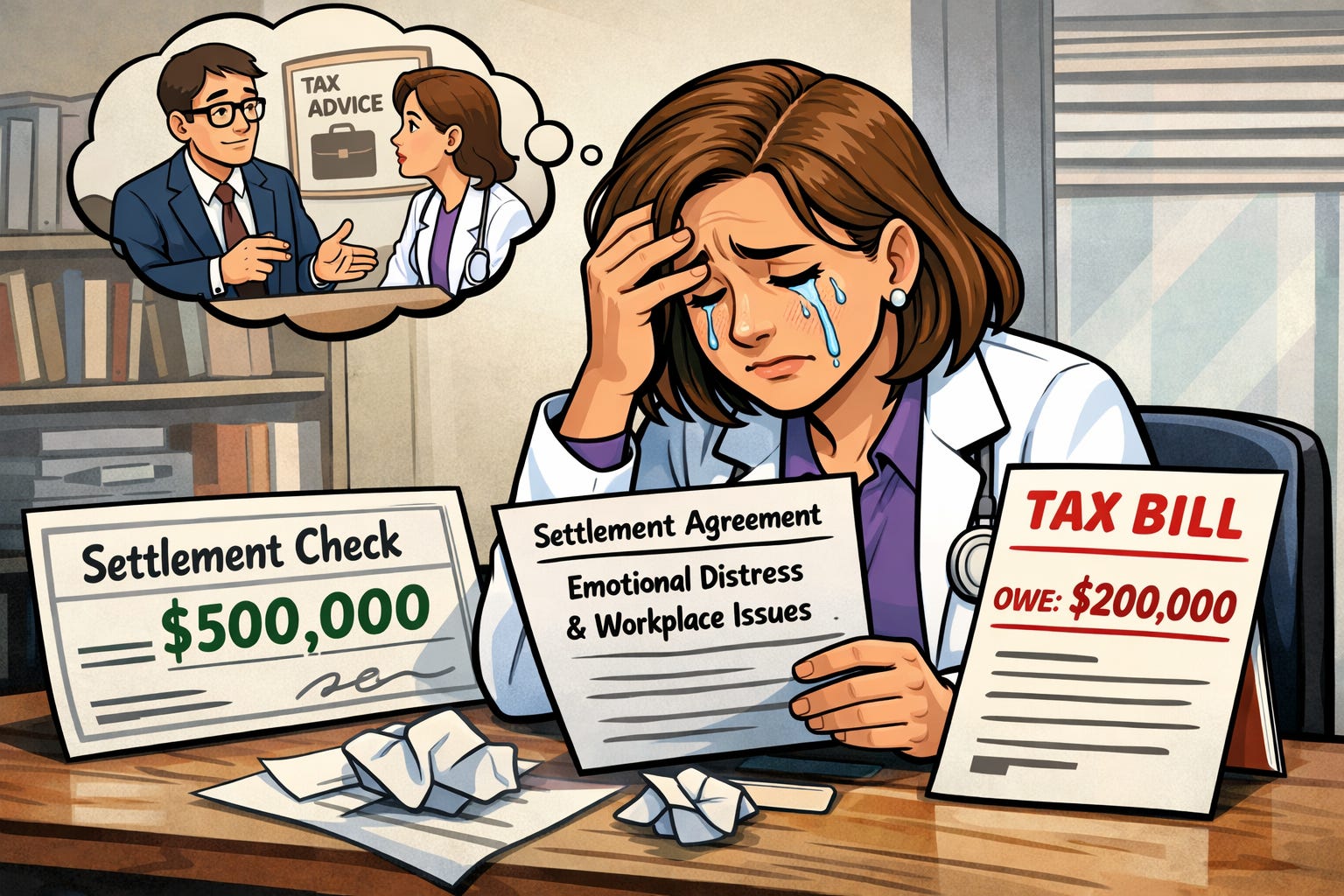

You receive a $500,000 settlement check.

You stare at it.

Two years of stress. Sleepless nights. Therapy. Feeling pushed out of a hospital you once trusted.

Finally… justice.

And then your CPA says:

“About half of this may go to taxes.”

Wait—what?

You paid the price.

Why is the IRS getting paid too?

Meet Dr. Neuro Logic

Dr. Neuro Logic is a neurologist with multiple sclerosis (relapsing-Remitting MS).

Brilliant. Dedicated. Quietly resilient.

But over time, something changed.

Whispers in the hallway. Subtle exclusion. Then not-so-subtle comments.

She believes it’s tied to her condition.

Her MS symptoms worsen.

Fatigue.

Headaches.

Anxiety.

Depression.

She spends thousands on therapy.

Eventually, she can’t take it anymore.

She quits. She sues.

Two long years later…

The jury agrees.

$500,000.

She wins.

She walks into her CPA’s office, smiling:

“This should be tax-free, right? After everything I went through?”

Her CPA reads the settlement agreement.

Silence.

Then…

“I’m sorry. This is mostly taxable.”

Her smile disappears.

“Why?”

The Rule That Feels Unfair

Here’s the uncomfortable truth:

The IRS does not tax your pain.

The IRS taxes what the money is for.

And that distinction changes everything.

Step 1: The Default Rule — IRC §61

Under §61, gross income means “all income from whatever source derived.”

The Supreme Court in Glenshaw Glass defined income as:

An accession to wealth

Clearly realized

Over which you have complete control

In plane english:

If you receive money that you control, from a completed event - you have income.

Dr. Neuro Logic received $500,000.

That’s income.

Unless…

An exception applies.

Step 2: The Exception — IRC §104(a)(2)

There is a powerful exception.

Under §104(a)(2):

Damages received on account of personal physical injuries or physical sickness are excluded from income.

If your settlement is for physical injuries or sickness → tax-free.

If not → taxable.

So the real question is:

What was Dr. Logic’s $500,000 actually for?

What Qualifies (and What Doesn’t)

Generally tax-free:

Damages for physical injuries (e.g., broken arm)

Damages for physical sickness (e.g., worsening MS)

Medical costs tied to those conditions

Generally taxable:

Lost wages or back pay

Interest

Punitive damages (almost always taxable)

Emotional distress (by itself)

Here’s the trap:

Emotional distress ≠ physical injury or sickness under §104.

Small exception:

You can exclude medical expenses for emotional distress (e.g., therapy)—but not the distress itself.

The Critical Doctrine: “Origin of the Claim”

This is everything.

The tax outcome depends on:

=> What the lawsuit was actually about

Not how you felt

Not what happened medically

But what the legal claim says.

Courts look at:

The complaint

How the case was argued

Settlement language

Payor’s intent

Key rule:

The tax result depends on the origin of your claim -

not what you later wish it said.

Why Dr. Logic Lost the Tax Benefit

She had:

Anxiety

Depression

Headaches

Worsening MS symptoms

But her case focused on:

Discrimination

Workplace retaliation

Emotional distress

Her settlement agreement?

It did not clearly say the payment was for physical injury or physical sickness.

IRS conclusion:

=> Employment + emotional distress case = taxable

The Dangerous Misunderstanding

A very common belief:

“If stress caused physical symptoms, the settlement should be tax-free.”

Not quite.

The IRS draws a hard line:

Emotional distress ≠ physical injury or physical sickness

Even if it causes:

Insomnia

Headaches

Stomach issues

These are treated as symptoms of emotional distress, not separate physical injuries or sickness.

A Real Case: Why Wording Matters

The taxpayer developed a real physical illness (shingles).

But:

The lawsuit focused on emotional distress

The settlement did not tie payment to physical injuries or sickness.

Result?

=> Taxable.

Same suffering.

Different wording.

Different tax outcome.

The Entire Game Comes Down to Words

If your settlement agreement says:

“On account of physical injury or physical sickness”

→ Strong path to tax-free

If instead it says:

“Emotional distress with physical manifestations”

→ Likely taxable

This can be the difference between:

$0 tax

vs.

$200,000+ tax bill

Why This Matters for Physicians

Doctors often experience:

Burnout

Hostile work environments

Retaliation

And real physical consequences:

Autoimmune flares

Shingles

Cardiac symptoms

But:

If your case is framed as employment stress instead of physical sickness

=> You may lose the §104 exclusion

Timing Is Everything

By the time the check hits your bank account…

The tax outcome is already decided.

Not by your CPA.

Not by your intentions.

Not by how much you suffered.

But by what was written—months earlier.

Once:

• Complaint is filed

• Settlement is signed

Your flexibility is gone

Because courts don’t ask:

“What actually happened to you?”

They ask:

“What did your legal documents say happened?”

They rely on:

The original story on paper (the “origin of the claim”)

Not the story you try to tell later

In other words:

You don’t win this battle after the lawsuit ends.

You win it when the lawsuit is written.

Same facts. Same pain. Different wording… completely different tax bill.

Final Thought

Dr. Neuro Logic didn’t lose because she didn’t suffer.

She lost because the law didn’t see her suffering the way her documents described it.

In tax…

Words = reality.

The difference between:

“Emotional distress”

and

“Physical sickness”

can be worth hundreds of thousands of dollars.

Pain may be unavoidable.

But taxes on that pain?

Sometimes avoidable — if structured correctly

If you’re ever in this situation:

Make sure your attorney and tax advisor align BEFORE signing anything.

Because in tax…

The story on paper is the only story the IRS hears.