The 2026 “Double Haircut” on Charitable Deductions for High-Income Doctors

Sadly, the new 0.5% AGI floor can wipe out the deduction entirely

Sorry to share a bad news for high-income doctors who itemize and give to charity every year.

Starting in 2026, the tax benefit of charitable giving gets squeezed in two different ways. One rule reduces the deduction from the bottom (a new “floor”), and another reduces the value of the deduction at the top (a new “cap”).

When you stack them together, your tax savings from charitable giving can be meaningfully smaller than what you were used to - and for smaller, routine gifts, the tax benefit could be close to zero. :(

Let’s walk through what changed and why.

What Changed in 2026

Two new provisions matter here:

a new 0.5% AGI floor for charitable deductions under IRC §170(b)(1)(I)

a new overall limitation on itemized deductions for top-bracket taxpayers under IRC §68(a), often described as the “2/37 rule,” which effectively reduces the value of itemized deductions to 37% to 35% for high-income taxpayers.

Let me unpack these with simple examples.

Mechanism #1: the “Bottom Haircut” (the 0.5% AGI floor)

Under IRC §170(b)(1)(I), charitable contributions are only deductible to the extent they exceed 0.5% of your contribution base (which is generally your adjusted gross income, AGI).

Said differently: the first 0.5% of AGI that you give to charity produces no current-year charitable deduction. It’s gone with the wind!

Assume that Dr. Linkin Park has AGI of $1M and makes $10,000 cash donation to his church in 2026 (and that’s his only charitable gift for the year).

AGI: $1,000,000

0.5% floor: $5,000

Cash gift: $10,000

Deductible amount: $10,000 − $5,000 = $5,000

So only half of that $10,000 gift is deductible. The first $5,000 does not generate a charitable deduction in the current year.

Quick nuance (so no surprises later): this floor applies to your total charitable contributions for the year, not separately to each donation.

Mechanism #2: the “Top Haircut” (Itemized Deductions capped at 35% value)

Beginning in 2026, IRC §68(a) limits the tax benefit of itemized deductions for taxpayers in the top (37%) bracket like Dr. Park.

In plain English: even if you’re in the 37% bracket (which you would be around $1M of income), itemized deductions - including charitable deductions - reduce your tax as if you were in a 35% bracket.

So instead of each $1 of charitable deduction saving you 37 cents in tax, it saves you only 35 cents.

Example:

If Dr. Park’s $10,000 charitable contribution were fully deductible (ignoring the 0.5% floor for a moment), it will reduce his tax by $3500, not $3700. That’s roughly a 5.4% reduction in benefit from this rule alone.

How the Two Rules Stack Together (A Lethal Combo)

Now, let’s combine both rules for Dr. Park’s situation

Assume:

AGI: $1,000,000

Cash charitable gift: $10,000

He is in the 37% bracket

Step 1: apply the 0.5% floor (IRC §170(b)(1)(I))

Amount disallowed by the floor:

0.5% of $1,000,000 = $5,000

Deductible amount:

$10,000 − $5,000 = $5,000

Step 2: apply the §68 cap (35% value)

Tax savings:

$5,000 × 35% = $1,750

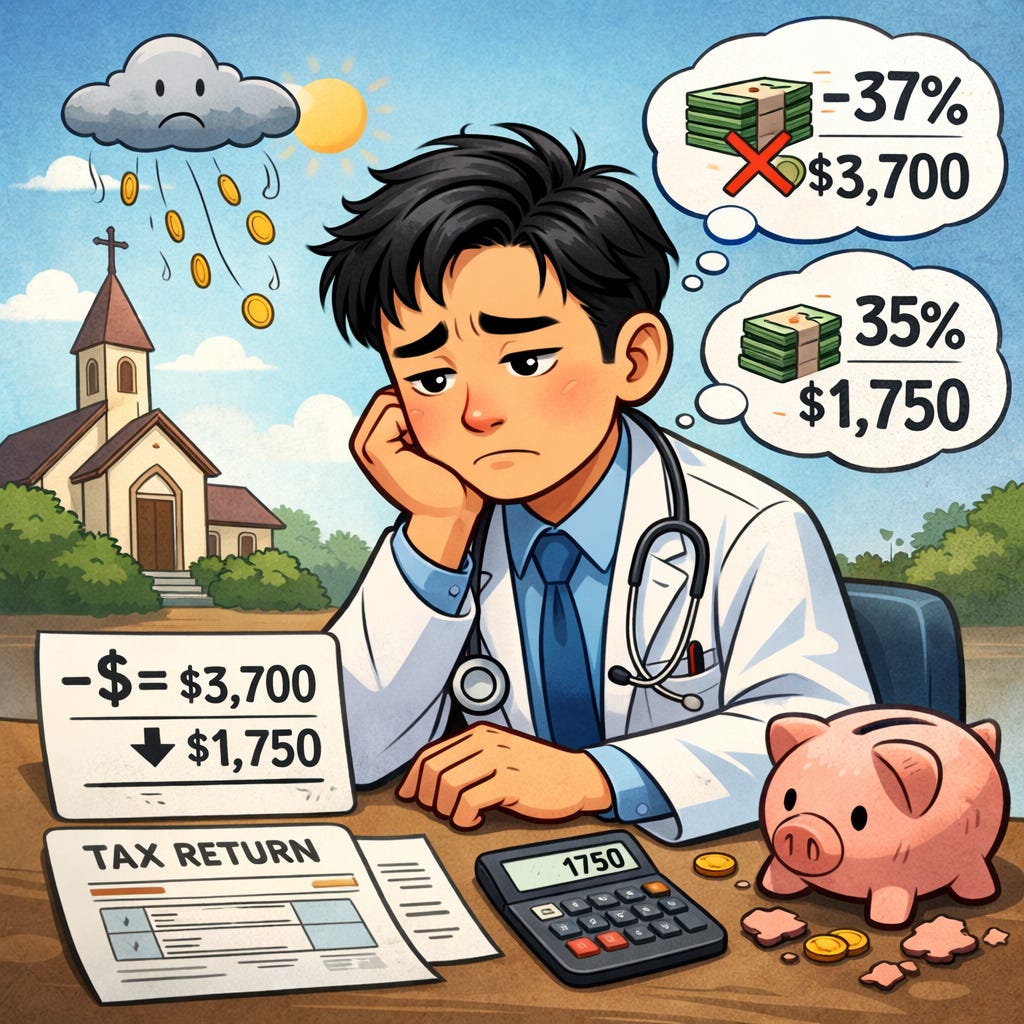

Because these changes by OB3, Dr. Park would have expected:

$10,000 x 37% = $3,700 of tax savings.

Now, the tax savings are only $1,750.

That’s a reduction of $1,950 in tax benefit - more than 1 50% drop for this size of routine annual gift.

For larger gifts (for example, $100,000 of charitable giving), the combined effect can work out to roughly a 10% reduction in expected tax savings compared to the old math.

Final thoughts

If you give because you’re generous (not because you’re chasing a deduction), you’ll probably keep giving.

But starting in 2026, high-income doctors who itemize should expect the tax benefit of charitable giving to be smaller than it used to be - especially for small routine annual gifts.

The key takeaway isn’t “don’t give.”

It’s this: know the new rules so you’re not surprised when the tax result looks worse than expected.