The $500,000 Ferrari Your Patient “Gifted” You

Why the IRS might call it income - not generosity

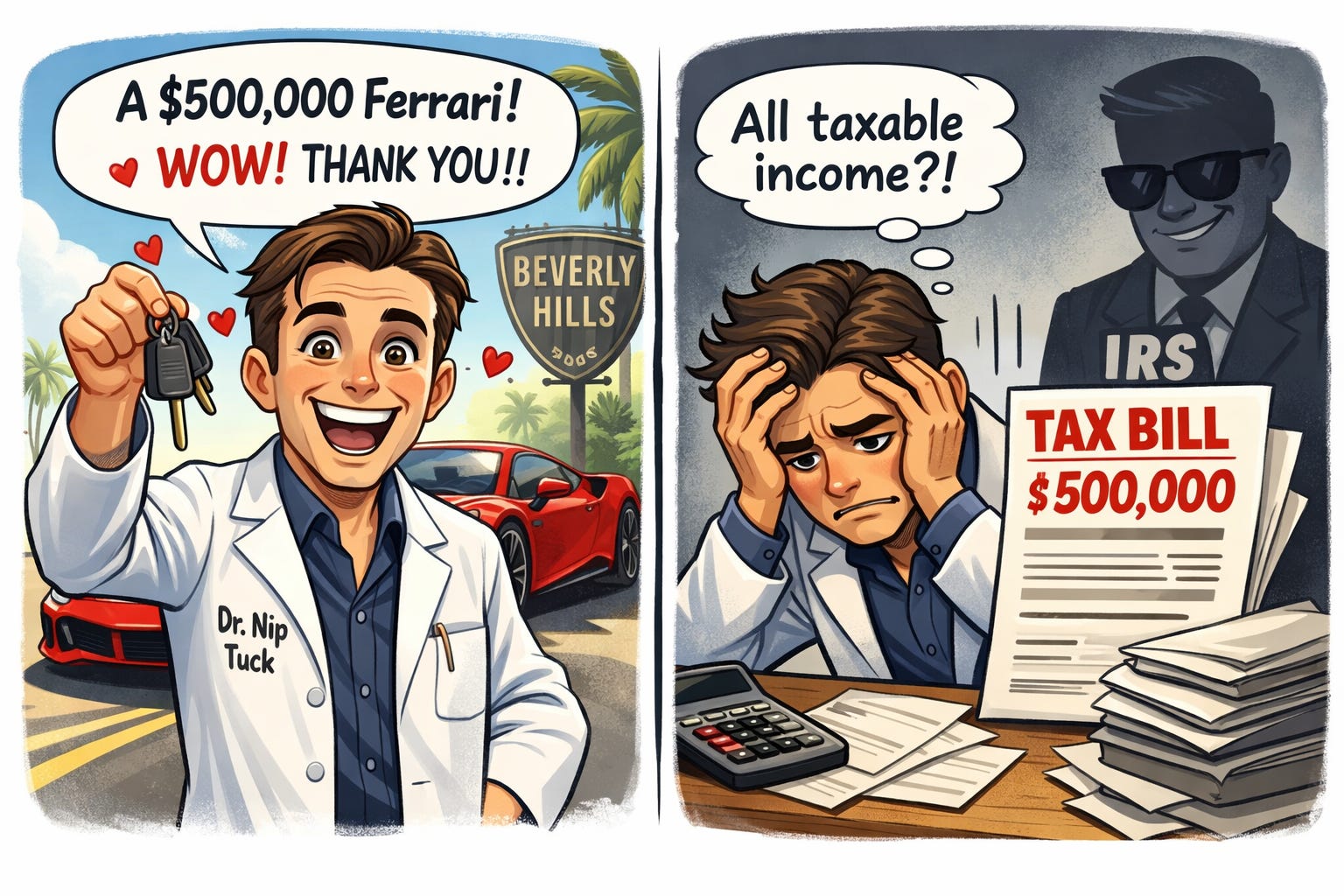

You’re a plastic surgeon, Dr. Nip Tuck, in Beverly Hills.

You just did a $20,000 rhinoplasty on Kimdashian.

She is ecstatic.

A week later:

“Doctor… this changed my life. This is for you.”

She hands you the keys.

A $500,000 Ferrari SF90 Stradale.

Wow. Unbelievable.

Before you celebrate, pause.

Do you report:

just the $20,000 of surgical fee …

or an additional $500,000 of income for the Ferrari?

Why This Gets Uncomfortable

Because the answer is:

In a professional setting like this, it’s almost always income.

Only in very narrow, fact-specific situations could you argue “gift.”

The Tax Framework You Need

Here’s a mental model:

IRC §61 → gross income includes everything you receive, unless income a specific exclusion applies.

IRC §102 → gifts are excluded - but only if they truly qualify as “gifts”.

So the entire question becomes:

Was the Ferrari a true “gift” under §102…

or compensation under §61?

The problem?

The tax code never clearly defines “gift”.

So we go to the Supreme Court.

The Supreme Court Standard (Commissioner v. Duberstein)

The Duberstein Court says:

A “gift” must come from:

“detached and disinterested generosity… out of affection, respect, admiration, charity or similar impulses”

And importantly:

You don’t just take someone’s word for it.

You look at the objective facts.

What “Gift” Really Means

A true gift is:

“Something for nothing” - no quid pro quo

No exchange

No expectation

Not “because you did this for me”

The moment it becomes:

“This is because of what you did…”

… then, it starts to look like income.

Apply it to Dr. Nip Tuck

Now plug in the facts:

A plastic surgeon.

life‑changing cosmetic surgery.

Paid $20,000

One week later: a new $500k Ferrari

Ask yourself, objectively:

Does that look like “detached generosity”?

Or a very large “thank‑you payment”?

Why the IRS is Skeptical

In professional relationships - doctor, lawyer, consultant

Transfers are usually not gifts.

They’re:

bonuses

tips

or extra compensation dressed up as generosity

The IRS starts from:

Default: everything is income under §61.

§102 is an exception - and interpreted narrowly.

In a doctor–patient setting, a big transfer right after treatment usually looks like compensation, not detached generosity.

Two Possible outcomes.

Version 1 - Likely IRS Position

“This is for the amazing work you did”

Professional relationship.

Transfer immediately after services.

Directly tied to the outcome

Motivated by gratitude for the procedure.

Result:

$20k rhinoplasty fee = income

$500k Ferrari = additional taxable income

This is compensation, not a §102 gift.

Version 2 - The narrow “Gift” Argument

To even argue gift under §102, you’d need very different facts:

A genuine, established personal relationship outside the medical context

No expectation of better service or access

No connection — explicitly or implicitly — to the procedure

Even then,

Duberstein requires looking at all facts and circumstances.

Calling something a “gift” doesn’t automatically make it one.

The Uncomfortable Truth

A thank‑you note doesn’t save Dr. Nip Tuck.

“I’m forever grateful” can still mean:

“I’m paying you more.”

Also:

“No legal obligation” ≠ “gift”

Voluntary payments can still be taxable income.

What the IRS Actually Focuses On

In practice, the IRS zeroes in on:

Timing (right after the procedure => strong compensation signal).

Relationship (professional => not naturally donative).

Intent (“why was this really given?”).

Substance (“does it feel like payment?”).

If it walks and talks like compensation…

It’s probably compensation.

Final Takeaway

The IRS doesn’t start neutral.

They start with:

“This is income.”

And you have to provide otherwise.

So in real life, for Dr. Nip Tuck:

Report the $20,000 fee, and

Report the $500,000 Ferrari as additional taxable income.

Unless you have very unusual, very clean facts.

Why This Matters

Same transaction.

Two theoretical tax outcomes.

But the difference isn’t what you call it.

It’s the facts, the framing…

… and what was true before the keys changed hands.

If you enjoy breaking down real-world tax traps like this, subscribe along.

Because these aren’t rare edge cases.

They show up more often than you think.